Have you written an application that issues invoices? Then you’ve probably struggled with PDF generation, for a start! (Headers don’t need to align, do they?) But there is much more to generating invoices than a pretty PDF. What information has to be on an invoice? How long should you keep an invoice?

Ms. Małgorzata Dankowska, a licensed tax advisor, is here to answer your questions. In this article, she’ll discuss the fundamental legal requirements for invoices in the European Union. In an upcoming article, she’ll explain some issues that are unique to electronic invoices.

Let’s start with the basics:

What Is VAT?

Value Added Tax (VAT) is a type of a consumption tax applied to the difference between something’s resale price and its purchase price. It differs from sales tax; at a given stage of turnover, only the added value (not the full turnover value) is taxed. This is achieved by imposing a full tax on sales (the Output VAT) but at the same time allowing a VAT deduction on the purchase (the Input VAT). Eventually, the full amount of the tax is borne by the end consumer, who is not entitled to use the Input VAT deduction.

For example: suppose a furniture warehouse sells a desk for 500€ net to a retailer. The retailer sells it to the customer for 700€ net. Applicable VAT rate is 23%. The warehouse must pay 115€ amount of OutputVAT on the sale, while the retailer must account for 161€ Output VAT on the sale being at the same time entitled to Input VAT deduction at the amount of 115€. All in all, the retailer must pay 46€ amount of the excess of Output VAT over Input VAT to the tax office. The customer pays the gross price of 861€ to the retailer and is not obliged to any further tax payments, but in fact bears the full VAT burden.

In the European Union, VAT is a harmonized tax. This means there are common legal regulations regarding VAT at the EU level. The fundamental legal act in this case is the VAT Directive (Directive 2006/112/EC on the common system of value added tax).

The European Union has different types of acts and regulations. Some of them are immediately enforceable as law in member states (like European Council regulations), while others need to be implemented into the member states’ legal systems (like directives). Directives very often do not set out specific actions that countries must follow. Instead, they state a desired result without dictating the concrete means each country will take to fulfill it.

Generally speaking, EU VAT law, being merely a directive, creates certain indications for the local governments. Each member state is responsible for the transposition of the directives into local law. However, if local regulations contradict the EU Directive, you can directly apply the Directive to your benefit.

What Is the Relationship Between VAT and Invoices?

In order to track the proper computation of VAT, the flow of goods and services within the EU needs to be well documented. Invoices are basic evidence of income generated, Output VAT calculations, and liability accounting; they’re also a major proof of VAT recoverability. They are crucial not only for VAT but also for income tax purposes. Hence, there is a range of requirements imposed by the EU as well as individual countries on the issuance of invoices.

Please Explain the EU VAT Directive vs. Local Regulations.

In the EU, invoices are regulated by the EU VAT Directive1 and local VAT laws. As the VAT Directive imposes straightforward regulations on invoicing, this should work the same in all EU member states. However, the Directive also provides some flexibility, so local authorities may decide on their own rules.

In short, invoicing regulations in one country may be a little bit different from the ‘standard’ EU format. Still, the standard format is a good place to start; you can modify it to match local specifics as the need arises.

What Are the General Requirements for EU Invoices?

Under EU regulations, an invoice is required in most business-to-business (B2B) transactions and in some business-to-consumer (B2C) transactions. As mentioned above, there may also be specific national rules about which transactions require an invoice.

In a B2B scenario, invoices are usually required when goods or services are supplied to another business or legal entity (such as an association or authority). There are some exceptions to this rule, though.

When selling to customers rather than other businesses, an invoice is generally issued in the following circumstances:

- In distance selling, when another EU country will collect the tax;

- When a new means of transport (some motorized land vehicles, vessels and aircraft as defined in the VAT Directive) is supplied to another EU country.

Member states may impose time limits on the issue of invoices when taxable persons are selling goods or services within their territory.

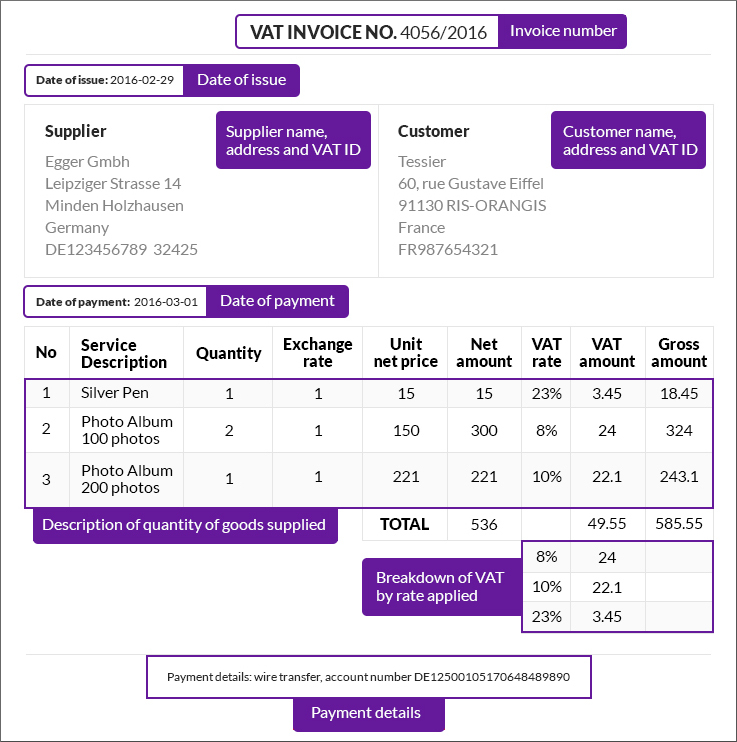

What Does Every EU Invoice Need?

The content of an invoice is primarily determined at the EU level; there are very few options for member states. Under EU VAT Directive, a full invoice must contain:

- The date of issue

- A unique sequential number identifying the invoice

- The supplier’s VAT identification number

- The customer’s VAT identification number

- The supplier’s full name and address

- The customer’s full name and address

- A description of the quantity and type of goods supplied OR the type and extent of services rendered

- The unit price of goods or services. This does not include taxes, discounts, or rebates unless these are part of the unit price.

- The transaction and payment dates (if these are different from the invoice date)

- The VAT rate applied

- The VAT amount payable

- A breakdown of VAT amount payable by VAT rate or exemption

- The foreign currency rate (if an alternative to the supplier’s national currency is used)

- The EU VAT Directive refers to sequential numbering, but this number can be based on one or more series. For example: if you run two online shops, you can choose different numbering schemes for each of them. These numbering schemes may include alphanumeric characters, which can help differentiate between types of customers, supplies, etc.

The choice of using a different series of numbers lies with the business.

Here we provide a sample data model showing the information related to a Full_Invoice, including the required Supplier and Customer information (VAT number, address), and the items that are on the invoice: Invoice_Item. As each item on an invoice may have a different VAT rate, we must have the VATRate per item in the Invoice_Item. Each Invoice is linked from a particular Customer_Order, once the order is finalized and an invoice must be created.

You will see that the information in the invoice tables is denormalized and kept separate from the volatile data in the many Customer – Address – Order – Product tables, so that the invoices are an exact “frozen” official, legal snapshot of the information that was present in the tables when the invoice was created.

What Additional Information Do Some Invoices Require?

In select cases, additional information is required on an invoice. Mainly, this would be due to the following conditions:

- A VAT-exempt transaction – include a reference to exempting legislation (EU or local)

- If a ‘reverse charge’ is applied to the transaction

- The intra-EU supply of a new means of transport (i.e. some additional information for a car)

- For margin schemes – include a reference to the scheme applied. (A margin scheme is a special VAT scheme available to travel agents and others.)

- If the invoice is “self-billing” (a customer issues the invoice instead of the supplier), those exact words must appear on the invoice.

- If a supplier uses cash accounting, the words “cash accounting” must appear on the invoice.

- For tax representatives: some VAT details may be needed if tax representatives are involved in a business. (Tax representatives are appointed by entities who do business in the EU but don’t have a physical presence there; they still need to settle VAT on their business activity.)

For example, if a Chinese manufacturer decides to sell their goods within the EU but does not establish a legal entity here (company, partnership, etc.), they still need to settle VAT in the EU. Depending on the member state, they may need to choose and appoint a tax representative (a person or company that fulfills certain conditions). The main goal of this is to ensure that the VAT is settled properly. The role of the tax representative is important, as they often have a joint responsibility for EU VAT liability. In practice, a tax representative service is often offered by specialized tax advisory companies.

In some cases, a simplified invoice can be issued. It must contain the following information:

- The date of issue

- The supplier’s VAT identification number

- The type of goods or services supplied

- The VAT amount payable (or information on how to calculate it)

- Where applicable, a specific, unambiguous reference to the initial invoice and the details that are being amended (on a credit note, debit note or other document treated as an invoice).

- The above points cover only the minimum information required. Providing additional information on an invoice is definitely allowed.

Electronic Invoices in EU Law

Electronic invoices are treated as equivalent to paper invoices under the VAT Directive. An electronic invoice, like its paper counterpart, must contain the same elements that we outlined above. In order for an invoice to be deemed as an e-invoice, it needs to be issued and received in electronic form. If an invoice is generated by accounting software, printed on paper and delivered to the client, it is not regarded as an e-invoice. The choice of the electronic format (XML, PDF, electronic fax, etc.) is made by the issuer. What is important is that the format ensures the authenticity of origin, the integrity of the content, and the legibility of the invoice from issuance until the end of the storage period.

Specific Invoicing Regulations

There are also some specific invoicing regulations for certain types of goods or services. For instance, when selling advisory services as a B2B transaction in the EU, it may be taxed according to the recipient’s (and not the seller’s) country. Such an invoice should literally contain the words “reverse charge”. To give another example, some countries may require invoices to be issued for VAT-exempt insurance and financial services, whereas others may not.

Another specific regulation relates to self-billing invoices. These may be issued by a customer for the goods or services they’ve purchased. The implementation of a self-billing system requires fulfilling further tax requirements. It will be discussed in one of the next posts.

How Long Should I Keep an Invoice?

The VAT Directive allows countries to impose their own period throughout which invoices need to be stored. Therefore, your storage time will depend on the member state where you reside.

The Directive also allows member states to require that invoices are kept in the form in which they were sent. In other words, paper invoices should be stored as paper, while e-invoices would remain in electronic form. The electronic storage of data guaranteeing origin authenticity, content integrity, and the legibility of the invoice also may be required for e-invoices.

Do Invoices Need to Be Translated?

EU regulations state that local tax authorities may require the translation of invoices solely for tax audit purposes (and they sometimes do). There are no specific European rules on the language of invoices, so in practice any national language may be applied. One quite popular solution is to have bilingual invoices: drafted in the local language and in English.

If you’re using an app-generated invoice, e-invoices are likely going to be your document of choice. In the next post, we’ll discuss electronic invoices in detail.

1 (Council Directive 2010/45/EU of 13 July 2010 amending Directive 2006/112/EC on the common system of value added tax)